1. Introduction:

In Ghana, the Income Tax Act, 2015, (Act 896), as amended, impose taxes on every person who earns income during the year of Assessment unless that person is granted an exemption under the law. In the case of individuals and partners in the partnership, their year of assessment is from the 1st January to the 31st December each year in line with the government calendar year. Income tax is payable for each year of assessment by an individual who has chargeable income for the year.[1] Thus, in Ghana, all income earners of a certain category have an obligation to register with the Ghana Revenue Authority, file their tax returns and pay taxes on their earnings.

Resident individuals who pay taxes are entitled to personal tax reliefs. The personal tax reliefs serve as an incentive and reduces the tax liability of such persons. There are many individuals who are ignorant of the personal tax reliefs under the income tax law. The law requires that tax returns be filed. In filing the tax returns, individuals are entitled to claim for these reliefs. Some of the reliefs can also be claimed upfront on monthly basis, provided the income is exclusively from employment.

The purpose of this paper is to examine the personal tax reliefs for resident individuals under the Income Tax Act, 2015, (Act 896), as amended.

The paper starts by explaining assessable income, chargeable income, resident individual and proceeds to analyse six (6) personal tax relief situations.

2. Assessable Income

The assessable income of a person for each year of assessment is the income of that person from any employment, business or investment.[2] The assessable income of a resident individual for a year of assessment from any employment, business or investment is the income of that person from each employment, business or investment for the year.[3] The income of a person from an employment, business or investment has a source in Ghana if the income accrues in or is derived from Ghana. The foreign source income of a resident individual is assessable to tax unless there is a law to the contrary. The assessable income of an individual is determined separately for each class of income. Thus, assessable income of an individual from business, employment or investment is calculated separately.

A resident individual is assessable to tax on the worldwide income basis. This means the resident individual is assessed to tax on income with a source in Ghana and outside Ghana. Hence the assessable income of a resident individual is the total income from any employment, business or investment for the year, wherever earned. A non-resident individual, on the other hand, is assessed to tax on income with a source in Ghana only, hence the assessable income of a non-resident is the income from employment, business or investment accruing in or derived by that non-resident individual from Ghana.

Illustration 1:

Godwin Addy was employed by Omega Limited in January 2018. He was paid GH₵30,000.00 as his annual basic salary. Godwin did not derive any other income from employment in addition to his basic salary in 2018. Godwin received a gross dividend of GH₵5,000.00f rom his investment at Alpha Limited in the year 2018. Godwin is also a businessman and operates a shop at Makola and made an income of GH₵8,000.00 in the year, 2018.

What will be his assessable income from Employment, Business and Investment for the year 2018?

From the above scenario:

The assessable income of Godwin from employment for the 2018 year of Assessment is GH₵30,000.00

Also, the assessable income of Godwin for the 2018 year of assessment from investment and business are GH₵5,000.00 and GH₵8,000.00 respectively.

3. Chargeable Income

The chargeable income of a person for a year of assessment is the total assessable income of that person for the year from each employment, business or investment less the total amount of deduction allowed that person.[4] The chargeable income of a person from employment, investment and business is determined separately.[5] Thus, a person can no longer aggregate income from employment, investment and business to arrive at chargeable income.

Illustration 2:

Using the scenario in Illustration 1 above and assuming that Godwin was granted allowable deductions of GH₵2,100.00 and GH₵1,200.00 in respect of his employment and business respectively for the year 2018 by the Ghana Revenue Authority, what will be his Chargeable income from employment, business and investment for the year 2018?

From the above scenario:

The chargeable income of Godwin from employment for the 2018 year of assessment is GH₵27,900.00 (that is, GH₵30,000.00 less GH₵2,100.00).

The chargeable income of Godwin from business for the 2018 year of assessment is GH₵6,800.00 (that is, GH₵8,000.00 less GH₵1,200.00).

In addition, since Godwin was not granted any allowable deduction in respect of the income from investment, the chargeable income of Godwin from investment for the 2018 year of assessment is GH₵5,000.00. However, dividend paid under a circumstance like this shall be subject to final withholding tax at the rate of eight percent (8%).

4. Who Is a Resident Individual?

A resident individual for tax purposes, in a year of assessment, means an individual who is[6]:

- a citizen of Ghana, other than a citizen who has a permanent home outside Ghana and lives in that home for the whole of that year;

- present in Ghana during that year for an aggregate period of one hundred and eighty-three (183) days or more in any twelve-month period that commences or ends during that year;

- an employee or an official of the Government of Ghana posted abroad during that year; or

- a citizen of Ghana who is temporarily absent from Ghana for a period of not more than three hundred and sixty-five continuous days, where that citizen has a permanent home in Ghana.

5. Personal Tax Reliefs and their Analysis

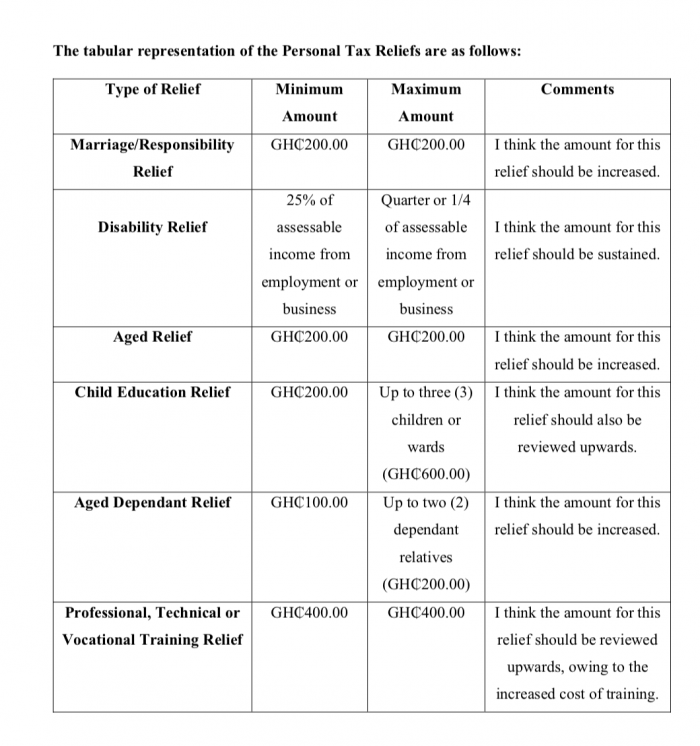

Personal tax reliefs are legally approved deductible allowances intended to reduce an individual’s chargeable income and thereby lessen the tax burden. It is intended to cushion the effect of tax on the individual and to make it bearable for them to pay the tax.[7] The personal circumstances of taxpayers are taken into consideration in granting these reliefs. For instance, a married individual with children attending school will normally have more responsibilities than an individual who is single. Therefore, in arriving at the chargeable income of a resident individual for the year of assessment, that resident individual is permitted to deduct personal tax reliefs from the assessable income for that year.[8] These personal tax reliefs are:

- Marriage/Responsibility Relief

- Disability Relief

- Aged Relief

- Child Education Relief

- Aged Dependant Relief

- Professional, Technical or Vocational Training Relief

It must be noted that a non-resident individual is not entitled to the grant of personal tax reliefs unless there is a provision in a double taxation arrangement to the contrary.[9]

It is noteworthy that Reliefs (i)-(iv) mentioned above can be claimed upfront on monthly basis provided the income is from employment only. Reliefs (v) and (vi) are however claimable upon filing of tax returns.

The analysis of the above-mentioned reliefs are as follows:

6. Marriage/Responsibility Relief

An individual who has a dependant spouse or at least two dependant children is entitled to a personal relief of two hundred currency points (GH₵200.00).[10] A dependant child or spouse means a child or spouse of the individual for whom that individual provides the necessities of life.[11] This relief is granted to only one spouse in a marriage after production of a marriage certificate or certified true copy of the registration of the marriage.

7. Disability Relief

An individual who has a disability is entitled to a personal relief of twenty-five percent (25%)of the assessable income from a business or employment.[12] The income of an individual with a disability, from an investment, is however excluded. A person with a disability means an individual with a physical, mental or sensory impairment including a visual, hearing or speech functional disability which gives rise to physical, cultural or social barriers that substantially limits one or more of their major life activities.[13] This relief is granted to individuals who prove to the satisfaction of the Commissioner-General that they are disabled.

8. Aged Relief

An individual who is sixty (60) years of age and above is entitled to a personal relief of two hundred currency points (GH₵200.00).[14] The individual in question must derive an assessable income during the year from an employment or business. Thus, that individual’s income from an investment is not included. The evidence of the date of birth of the individual in question must be provided.

9. Child Education Relief

An individual who is sponsoring the education of a child or ward in a recognized registered educational institution in Ghana is entitled to a personal relief of two hundred currency points (GH₵200.00) per child or ward up to a maximum of three children or dependents.[15] This relief may be claimed in respect of three (3) children or wards amounting to a total of six hundred currency points (GH₵600.00). The Commissioner-General shall grant only one relief where two or more persons qualify in respect of the same child or ward.[16]

It must be noted that the children or wards of the individual in question could be biological or otherwise. There must be evidence that the individual claiming the relief is funding the education of those children or wards. There must also be evidence that the children or wards are studying in that educational institution. A certificate issued by the Head of the educational institution concerned stating that the child or ward is studying at that institution and that the individual is responsible for sponsoring the child or ward’s education will suffice.

10. Aged Dependant Relief

An individual who has a dependant relative, other than a child or spouse, who is sixty (60) years of age or more is entitled to a personal relief of one hundred currency points (GH₵100.00) but that individual may only claim relief in respect of two dependant relatives.[17] A dependant relative means a relative of the individual for whom that individual provides the necessities of life.[18] The Commissioner-General shall grant only one relief where two or more persons qualify in respect of the same relative.[19] This relief may be claimed in respect of two dependant relatives. Thus, the total amount that may be claimed is two hundred currency points (GH₵200.00). Resident individuals will enjoy this relief if they prove to the satisfaction of the Commissioner-General that they have an aged relative who is dependent on them.

11. Professional, Technical or Vocational Training Relief

An individual who has undergone training to update his professional, technical or vocational skills or knowledge is entitled to a personal relief which is equivalent to the cost of the training of not more than four hundred currency points (GH₵400.00).[20] Anyone who wishes to claim this relief must provide evidence to the satisfaction of the Commissioner-General that the individual has undergone training to update his professional, technical or vocational skills or knowledge.

12. How to apply for the reliefs.

An application can be made to the Commissioner-General for the reliefs using the prescribed form. The relief form can be obtained from any of the Domestic Tax Revenue Division offices of the Ghana Revenue Authority across the country.

13. Recommendations

Tax reliefs are designed to encourage voluntary tax compliance. However, many people or taxpayers are unaware of these reliefs. It is recommended that the Ghana Revenue Authority should engage in an extensive education of the public or taxpayers on these reliefs and the tax laws in general in line with its function of promoting voluntary tax compliance and tax education.

It is also recommended that the amounts for Marriage/Responsibility Relief, Aged Relief, Child Education Relief, Aged Dependant Relief and Professional, Technical or Vocational Training should be increased. This call for an increase is premised on the fact that these amounts have been overtaken by the rate of inflation and related cost of living over the years and are thus not meeting their intended purpose, that is lessening the tax burden on the taxpayer. It may be argued that some people may not bother to file their tax returns and claim the reliefs due to the amount of money which is being granted as a relief per annum.

14. Conclusion

Personal tax reliefs are legally approved deductible allowances intended to reduce individual’s chargeable income and thereby lessen the tax burden. It is intended to mitigate the effect of tax on the individual and to make it bearable for them to pay the tax. Marriage/Responsibility Relief, Disability Relief, Aged Relief, Child Education Relief can be claimed upfront provided the income is exclusively from employment. Aged Dependant Relief and Professional, Technical or Vocational Training Relief are however claimable upon filing of tax returns. All resident individuals are therefore encouraged to take advantage of these reliefs, file their annual tax returns and claim the reliefs accordingly.

Aknowledgment: I am very grateful to Mr. Abdallah Ali-Nakyea, Managing Partner of Ali-Nakyea & Associates, Accra; Dr. B.D. Kofi Henaku, the Chief Executive Officer of Henson Geodata Technologies-Accra and Mr. Dominic Dokbilla Naab, Head of the Training and Development Department of the Ghana Revenue Authority-Accra and others who reviewed and commented on this paper. This paper would not have been completed without your contribution. All mistakes, errors and blunders are my responsibility.

[1]See section 1(1)(a) of Act 896

[2]See section 3(1) of Act 896

[3]See section 3(2)(a) of Act 896

[4]See section 2(1) of Act 896

[5]See section 2(2) of Act 896

[6]See section 101(1) of Act 896

[7]Abdallah Ali-Nakyea, Taxation in Ghana; Principles, Practice and Plaining, 3rdedition, page 107.

[8]See section 51 of Act 896

[9]See Regulations 2(a) of L.I. 2244 of 2016

[10]See paragraph 1 (a) of the Fifth Schedule to Act 896

[11]See paragraph 3 of the Fifth Schedule to Act 896

[12]See paragraph 1 (b) of the Fifth Schedule to Act 896

[13]See section 59 of Persons with Disability Act, 2006 (Act 715)

[14]See paragraph 1 (c) of the Fifth Schedule to Act 896

[15]See paragraph 1 (d) of the Fifth Schedule to Act 896

[16]See paragraph 2 of the Fifth Schedule to Act 896

–

[17]See paragraph 1 (e) of the Fifth Schedule to Act 896

[18]See paragraph 3 of the Fifth Schedule to Act 896

[19]See paragraph 2 of the Fifth Schedule to Act 896

[20]See paragraph 1 (f) of the Fifth Schedule to Act 896

Leave a Reply